From the potential of 5G to the power of AI and more, our connected lives are being shaped by the growth of transformative technologies. Powerful on their own, these transformative technologies are now converging to change fundamentally how we interact with the world, how we do business, and even how we communicate with each other. As this convergence continues, formerly separate industries are intersecting in new ways, with new opportunities (and challenges) emerging.

Evolution of transformative technologies:

Market and technology capabilities continuously drive innovation

Transformative technologies enable shifts in how enterprises function and how individuals live everyday life. As technologies become smarter and more sophisticated, and as markets evolve, transformation can begin in new industries. The rate at which we see these technologies take hold has grown rapidly in recent years.

Major trends for 2019

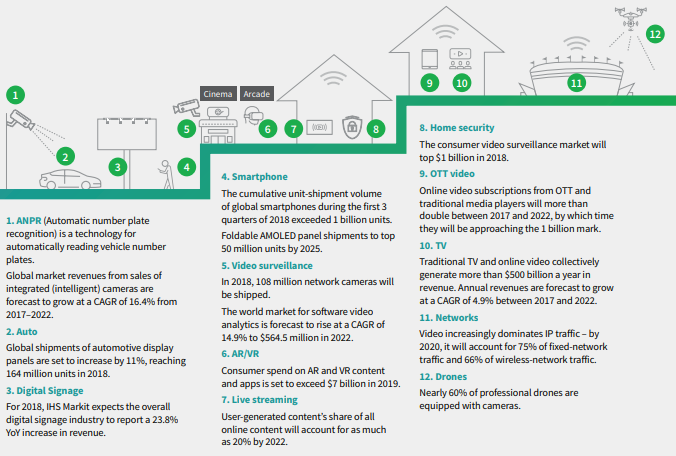

Trend 1: Video Everywhere

Video’s increasing ubiquity is forcing significant industry change as a growing number of players vie for consumer attention and revenue, and businesses adapt to cope with the rising demand.

Driving forces for Video Everywhere trend include the rise of online offerings and platforms, including those from powerful new market entrants; increasing penetration of mobile connected devices capable of capturing and displaying video; advances in network and transmission technologies for sharing it; and the resultant explosion of user-generated content and social video.

The trend affects not only media sectors such as TV, home entertainment, social media and games, which are at its heart, but other industries including security, education and healthcare as well that are becoming increasingly reliant on video technology.

However, the Video Everywhere trend poses certain challenges that need to be resolved.

Infrastructure, network capacity, and user experience

Challenge: Current generation network infrastructure is not equipped to support the rapid rise in video traffic.

Solution: Next-generation network investment is essential for supporting a reliable, high-quality user experience for a mass user base. 5G will be transformative for video, introducing the massive mobile broadband that will enable streaming of professional video and user-generated content at scale.

Content and monetization

Challenge: Service providers, broadcasters and platforms competing for a share of video revenues need the right mix of quality content, an expensive commodity that can be difficult to effectively monetize for a good return on investment.

Solution: Investment in programming, whether exclusive or acquired, should be proportionate to a video provider’s ambitions and serve clear strategic objectives. Content services, features, and video-specific network access can all be monetized to varying degrees, but video can also serve bigger-picture goals. For telcos and bigtech firms, in particular, it attracts users to a bundle of services that collectively drive revenue and EBIDTA growth and boost customer stickiness. Video should therefore be positioned as a primary tool for elevating the overall value proposition.

Privacy and data protection

Challenge: Increasing video capture in daily life – whether from smartphones, wearable devices, drones, or satellites – will result in more and more images of private citizens being gathered, stored, and potentially shared. Advances in artificial intelligence and machine learning, meanwhile, are enabling facial-recognition-based identification, potentially putting people’s privacy at risk.

Solution: Governments and regulators must play a key role in protecting citizens, putting the appropriate policy, legislation, and tools in place to prevent breaches of privacy and data protection.

Strategies of consolidated media and telco players to take shape in 2019

Fuelled in part by a fear of the threat posed by the likes of Netflix, Amazon, Google, Facebook, and Apple, a spate of significant M&A activity in the media and telecoms industries has seen key players merge and expand. The impact of major deals involving AT&T and Time Warner, Disney and Fox, Vodafone and Liberty Global, and Comcast and Sky, respectively, will begin to become apparent in 2019, as the strategies of newly enlarged industry leaders take shape.

Trend 2: The Edge

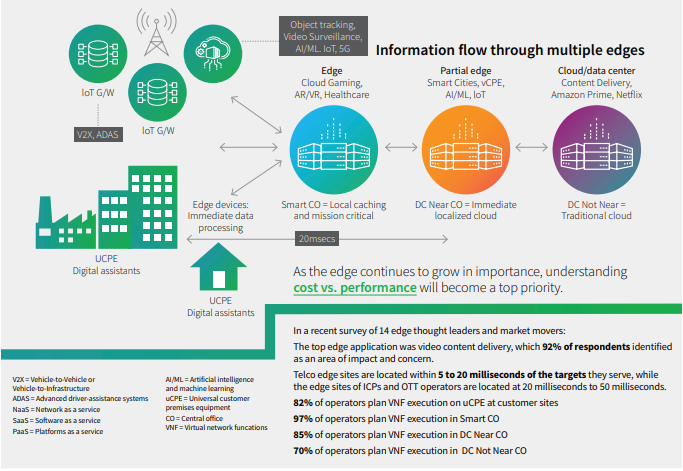

The Edge broadly refers to processing traditionally performed in a cloud environment that is now being run closer to either the sensor data or the human-machine interface. It is changing the way networks are being deployed and devices are being built, plus enabling new revenue streams as compute resources are available closer to the end consumer.

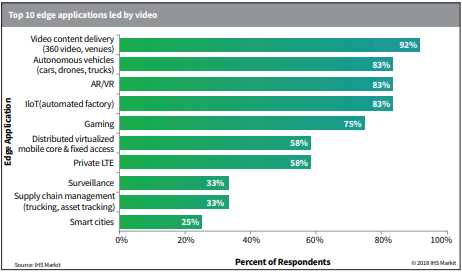

Driving forces for the Edge trend include – the top edge application is video content delivery; real-time or low er latency for time-critical workloads or safety applications; resiliency for situations where the network connection is not optimal or offline; data aggregation and the ability to filter in order to balance storage, networking, and compute; and security and privacy functionality centralized and enhanced – particularly in the IoT domain where end nodes might not be capable.

The trend affects service providers, cloud providers, and IoT companies that are particularly centered in the edge discussion. The edge also impacts the entire value chain from semiconductor providers through OEMs to segments like media, security and gaming.

The evolution of edge

The emerging edge is a new and powerful set of locations for handling applications, and the edge can be anywhere. For example, a connected car is an edge on wheels. With so many target locations possible, some edge solutions will be built to handle less data for fewer users while others will be large and handle massive datasets for many users, including data centers distributed around a metropolitan area. New low-power, specialized chips will power edge devices, and while many people equate the edge with 5G, the edge and edge apps exist today, yet there have been very few 5G deployments to date.

As the IoT universe expands to include more devices – some 20 billion units, according to IHS Markit estimates – the sheer scale of data generated in the future will render the current paradigm of a centralized cloud untenable. IoT edge processing saves upstream traffic and bandwidth by turning huge amounts of raw data into immediately usable decisions and directives to feed back to objects and devices downstream, and a much reduced and refined set of data to send upstream to data lakes and other decision-making systems.

Barriers to edge deployment

The main obstacle to effective edge deployment is the large bandwidth required. The most significant issue is the need to reduce upstream traffic via analytics in order to manipulate and refine data at the edge.

Technical considerations and high cost are also barriers to edge deployment, according to survey respondents. In fact, many edge apps require new software to be invented, but no common application program interfaces (APIs) currently exist for edge app developers, and for a robust edge to exist, a common developer platform is needed. There is, however, potential in the open-source Eclipse platform of APIs and microservices.

Also at stake is the question of how an operator can manage, monitor, operate and control thousands of edge sites, since no standard software stack exists. Another issue for automation is how to translate data from big data lakes and develop the ‘small data’ artificial intelligence inference engines required to work at edge venues. More experimentation and experience are needed to determine suitable and appropriate business cases for the edge.

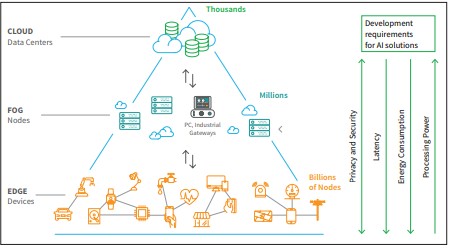

Trend 3: Artificial Intelligence (AI)

Implementation scenarios: edge, cloud, and hybrid

As the future unfolds and technology rapidly advances, AI will eventually touch all industry domains and transform our world. Machine learning, neural networks, and deep learning all fall under the AI umbrella.

The development of new algorithms and methods to enhance efficiency and problem-solving capabilities are driven by the high complexity of several applications and the prevalence of big data. For AI to fully develop, there remain many components and driving forces that must mature, advance, and succeed.

The trend is driven by forces that include the ability of machines to become more independent and autonomous, learning from their surroundings, the explosion of collectable and analysable data through numerous platforms – from mobile to cloud, high-performing electronics able to elaborate huge amounts of data and extract structured knowledge, availability of adjacent transformative technology creating the perfect storm – connectivity, IoT, and cloud.

The pervasiveness of AI is not expected to have borders. Every industry and the entire society will benefit from AI, but we need also to adapt to such disruption. Automotive, consumer electronics, security, education and healthcare are becoming increasingly reliant on AI.

AI at the edge vs. AI at the cloud

The speed of development in AI, and more specifically in domains like machine and deep learning has aided the adoption of AI in several industries including consumer electronics, healthcare, industrial and automotive. We are at the beginning of an industry revolution. AI is currently implemented on end-point devices, at the edge of the network, or in the cloud. Hybrid combinations are also suitable for certain applications. Each approach comes with its own use cases, specific requirements, and performance needs.

In particular, cloud AI will allow more computing power to analyze data and utilize more complex algorithms (such as deep learning), possibly close to where the training data is gathered. There are, however, potential issues around privacy, latency, and stability. A stronger on-device or edge implementation of AI algorithms will help offset those concerns to some degree while offering other advantages required by a broad range of applications.

The expectation is that cloud will have a huge advantage to tackle training sessions for artificial neural networks (ANN) or deep learning network types, where centralization of data and massive computation are required. Edge devices will be much more suitable for inference applications, whether end-point devices or edge network systems.

Technology insights in key areas

Transformative technologies are impacting markets all over the world, and recent developments in key markets will be driving forces in how technology grows and converges in 2019. IHS Markit provides syndicated market research, advisory services, as well as cost and performance benchmarking services for every aspect of the supply chain for each of these transformative technologies.

5G: What are service providers up to?

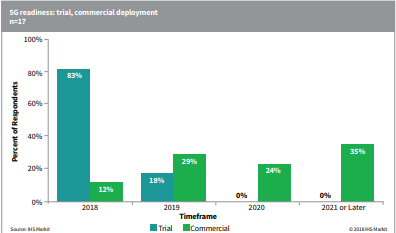

According to the IHS Markit Evolution from 4G to 5G: Service Provider Survey, 82% of mobile operators respondents are busy with trials and testing of 5G technology. This activity is mainly in North America and Asia, with 12 percent – all from North America – planning commercial 5G rollouts by year’s end.

82% of mobile operator respondents rated ultra-low latency (ULL) the chief technical driver for 5G, followed by decreased cost per bit (76%), and increased network capacity (71%). Every technical aspect related to substantial improvement in network performance such as lower latency, higher capacity, higher bandwidth, and higher throughput, while decreasing the cost per bit continues to receive high ratings in our survey. This survey outcome is logical because these considerations are the foundation of the 5G definition.

Meanwhile, the most challenging network development item on the 5G agenda is radio. 53% of operator respondents said radio is the area of the network that will require the biggest development effort to make 5G happen, followed by transport (24%) and management (14%).

Enhanced mobile broadband (eMBB) was the highest rated 5G use case driver among survey respondents, followed by real-time gaming. As real-time gaming requires a super-fast network with low latency, it cannot occur in the absence of eMBB; the same applies to high-definition (HD) and ultra-high-definition (UHD) video services and tactile low-latency touch and steer. Even so, respondents expect fixed-wireless access (FWA) to be ready for commercial deployment first.

The bottom line is early 5G will be an extension of what we know the best – broadband, whether in FWA or eMBB form. Don’t expect factory automation, tactile low-latency touch and steer, or autonomous driving to be ready on 5G anytime soon despite being touted as the chief 5G use cases.

Blockchain: Nascent today, but opportunities for cost savings and efficiencies are sky-high

While still nascent today, blockchain business value, which refers to the cost savings and efficiencies that could be realized by incorporating blockchain into corporate business strategies, is projected to increase from $2.5 billion in 2017 to $2.0 trillion in 2030.

Although blockchain is still an emerging technology, it is expected to be transformative. According to the Blockchain vertical opportunities report from IHS Markit, this technology demonstrates especially significant potential across the following vertical industry markets and application areas:

Financial

The financial vertical market, which includes financial services, insurance, and financial technology (fintech), will primarily use blockchain to conduct cross-border payments, share trading, securities, claims management, derivatives, asset custody across both public and private markets, currency, collateral management, and corporate actions processing. Because the market capitalization of all the world’s stock markets is equal to $73 trillion, even small cost savings and efficiency gains can lead to significant business value for companies and industries that decide to introduce blockchain technology.

Supply chain and logistics

The supply chain and logistics industry is projected to improve significantly with the introduction of blockchain technology. Indeed, the World Trade Organization (WTO) estimates that the reduction of barriers throughout the supply chain could potentially increase global gross domestic product by 5% and escalate total trade volume by 15%.

Identity management

With the projected increase in the number of blockchain projects that are launched and become commercially deployed, the business value within the identity management sector is projected to reach $200 billion by 2030. The ID2020 initiative continues to promote and support blockchain technology to help the 1.1 billion people who live without an officially recognized identity.

Retail and e-commerce

The initial uptake of blockchain in retail and e-commerce is projected to be led by trade promotions, decentralized marketplaces, payments, smart contracts, supply chain, and other applications. With the increase in the number of blockchain projects that are launched and become commercially deployed within this vertical sector, the business value is projected to reach $164 billion by 2030.

Healthcare

In the United States alone, counterfeit drugs cost pharmaceutical companies more than $200 billion annually in lost revenue. Blockchain could potentially help to minimize these losses. For this and other reasons, the business value from blockchain in the healthcare sector is projected to reach $134 billion by 2030. The initial adoption of blockchain within the healthcare sector is happening in the application areas of medical data management, drug development, claim and billing management, and medical research.

AI advances in virtual assistants and HMI

Several companies have been focusing attention on AI, and more specifically on functionalities that today already have an impact on daily life, like the human-machine interface (HMI).

Google, Apple, Microsoft, Amazon, Tencent, Huawei, Samsung, and others are investing heavily to improve and to provide best-in-class performance in applications like virtual assistants and natural voice recognition.

Recently, Google Duplex was introduced during the Google I/O event. This was just a couple of days after Microsoft announced the acquisition of Semantic Machines in a move aimed at boosting its AI capability into HMI applications with in a more natural interaction. Semantic Machines’ competence is expected to add significant value to Microsoft’s platforms through Cortana digital assistance and Xiaoice social chatbot.

Last but not least, and echoing Google and Microsoft, Apple also hinted at new voices and features for Siri that was announced in its developer’s forum, WWDC 2018.

The human touch

HMI is a basic application that is extremely powerful. HMI, by definition, can be deployed in multiple applications and in several industries and domains, from consumer and mobile electronics to automotive, passing through smart home and appliances or industrial. Wherever humans need to interact, an advanced HMI will be able to add value.

Although Siri, Alexa, and Google Assistant have been developed for consumer electronics applications, we already see these companies trying to expand their digital assistant and interface into other domains, including smart homes and even the automotive industry.

Taking the automotive sector as an example, it is well worth considering that even assuming the rapid availability of AI and ‘self-determining’ technologies, legal aspects are likely to slow the whole implementation process, especially for safety-critical applications. OEMs will be subject to much greater liability if machines are to take over the role of humans as is anticipated in the self-driving car. Nonetheless, in the same automotive domain, in-vehicle HMI for speech and gesture recognition exhibited a fast introduction of AIbased algorithms with immediate advantages for drivers.

From the competitive landscape perspective, it is interesting to note that Google, as well as Amazon and other West Coast US players, have a strong footprint in Europe and America, but their presence is very limited in the fast-growing Chinese market. Digital assistants from local Chinese technologies companies – Baidu, Alibaba, Tencent, Huawei, Xiaomi, and the like – are better placed to succeed than their Western counterparts for geo-political reasons as well as for their specific language competence.

Google and Amazon are, in fact, largely absent from the Chinese market, and while Apple is present with Siri, it offers only relatively limited functionality. This is in part a result of Apple’s more closed approach to integrating with third-party developers and because of other limitations around Siri’s functionality for specific use cases. Samsung also has a limited share in China; it did not include Chinese language support at Bixby’s launch, and this only came at the end of last year.

Advances in AI in digital assistants hope to increase voice usage

Digital assistants and AI look to be in a perfect symbiosis and are fast developing. The basic business case of HMI is straightforward, enabling and augmenting user interaction with machines. However, according to a recent survey from IHS Markit, despite extensive marketing of smart home devices that can be controlled via voice, less than a quarter of users use voice to control these devices. Smartphone app-based control of smart home devises is not going away.

Advances in digital assistants will also create new business cases, which might be less related to fast and comfortable user experience, but directly associated with revenue growth and/ or cost reduction. Natural language skills will allow an improvement in customer support and interaction, enabling personalized feedback on new offers/ products that might better suit customers’ needs.

In today’s connected society, digital assistants are making our lives more convenient and paving the way for smarter and more connected communities. Digital assistants are also creating massive revenue opportunities for businesses both big and small.

With adoption rates for digitally assisted voice-command products like smart speakers growing exponentially, competition in the market is fierce and companies will need to optimize product launches, discover areas for improvement, and improve costs.

Next-generation cloud gaming

Against a backdrop of burgeoning spend on streamed entertainment content, a new wave of commercial interest in cloud gaming emerged in 2018, driven by new technologies and new business models, and by major technology and internet companies seeking to make a mark on the games sector value chain, called ‘next-generation cloud gaming.

The market and technological conditions to make cloud gaming successful are now more aligned than ever, and with commercial services from Google and Microsoft predicted to launch in 2019, IHS Markit expects the technology to make a meaningful impact on the $145 billion games market during the year.

The cloud gaming value chain offers up commercial opportunities to a cross section of the biggest technology, internet and content companies. These companies include cloud service providers, telcos, consumer electronics companies, big media companies, and games publishers. Additionally, cloud gaming is closely linked to other broader technology trends – GPU computing in the cloud, ubiquitous video, PC virtualisation, and 5G rollout.

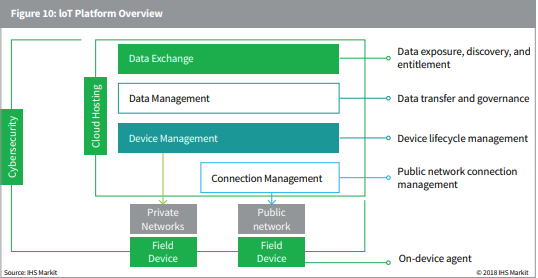

IoT: Making app development simpler

Application enablement platforms (AEPs) are an IoT platform segment that facilitate IoT device and data management. IoT application developers and adopters increasingly use AEPs across a range of industry verticals to simplify IoT application development and management. While AEP vendors initially focused on providing the features and functions common across all IoT applications – and comprising roughly 80% of application code base – many vendors are extending their offerings into specific vertical solutions, especially for connected cars, smart cities, and industrial automation.

IHS Markit forecasts a 38% CAGR from 2017 to 2022 for the rise in the cumulative number of IoT devices under management by an AEP, rising to 6.7 billion devices under management by 2022. Likewise, we project a 33.1% CAGR in the growth of annual AEP revenue over the same period, growing to $83.0 billion in 2022. This growth is enabled by the increasing adoption of IoT solutions across a range of industries and use cases, coupled with the growing desire of many customers to outsource as much IoT development as possible in order to focus on core competency aspects of their business.

The number of new AEPs introduced to the market held steady year over year until 2009, then new AEP introductions peaked at 44 introduced in 2015. However, since that time, the number of new AEP introductions has declined sharply, and the number of AEP vendor exits (through acquisition or by closing operations) started to increase in 2011, peaking in 2017.

According to IHS Markit, consolidation will happen for two key reasons – first, there is a market perception of there being too many platforms that are undifferentiated from each other; second, especially since 2014, many very large infrastructure vendors have entered the AEP market. These new vendors could potentially acquire other AEP vendors and greatly increase competitive pressure on the remaining vendors.

A principal AEP vendor concern is the degree of uncertainty concerning how best to price AEP offerings. Generally, device management functionality is priced around $0.50 to $1.00 per device per month, while data management functionality is priced around $0.20 per device per year. However, owing to the wide variability in the specific features and functionality offered, whether the monetization model is consumption-based, value-oriented, or revenue share, and the type of AEP vendor (e.g., cloud infrastructure vendor versus platform specialist), there is wide variability in the actual pricing any customer will receive. Furthermore, customers view pricing models as overly complex and difficult to resolve.

The IHS Markit Application enablement platforms report 2018 tracks the AEP segment of the IoT platforms market. The report includes worldwide and regional market size, forecasts through 2022, and an analysis of key technical and market trends influencing the growth opportunity in the AEP segment.

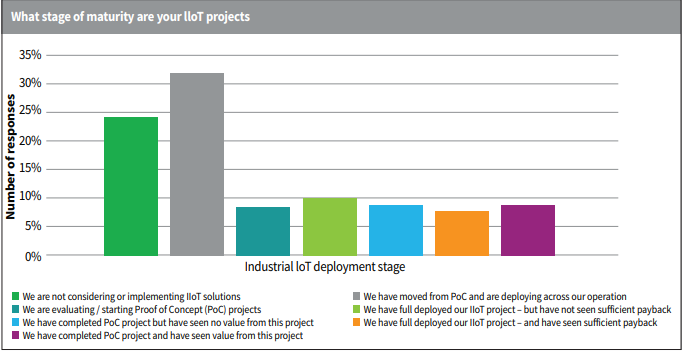

Is industry ready for IoT?

According to the Industrial IoT readiness survey 2019, although the industrial sector saw a significant increase in both proof of concept (PoC) and full deployment industrial IoT (IIoT) projects in 2018, over half of all end-users have yet to trial industrial IoT solutions. Moreover, among those that have success has been mixed with only slightly more than half of projects having shown value. In many cases, this has been as a result of poor project scoping and implementation.

In 2019, we expect to see a continued increase in the number of both PoCs and deployments, as well as an increase in deployments showing a payback.

As well as implementing best practices, companies must also evaluate areas where investment might be needed to become ‘IIoT ready.’ This includes upgrading legacy equipment and networks that may have been in place for decades, evaluating the processes for collecting, storing, and applying meaning to data; training existing workers to adopt new practices based on data collected from manufacturing processes; and reconsidering how products and services are bought and sold as new business models emerge.